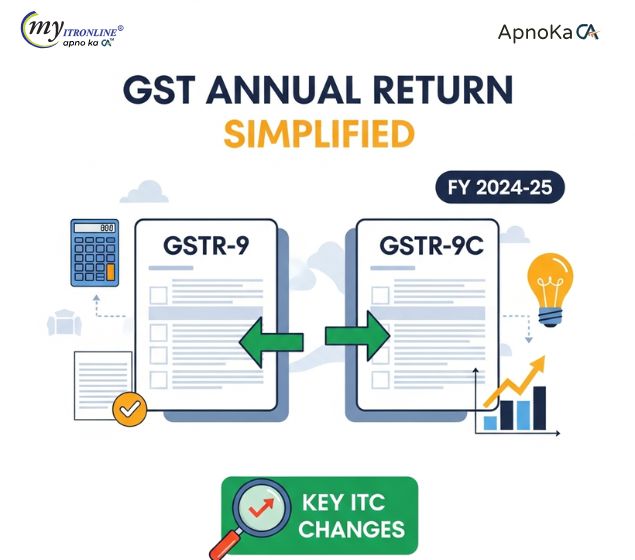

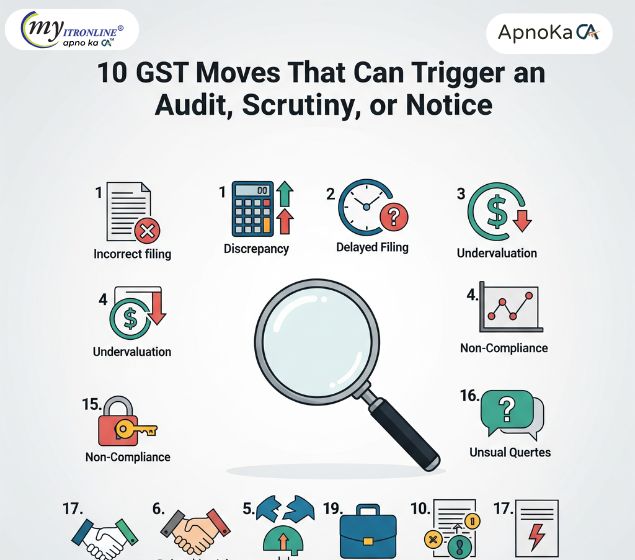

GSTR‑9 Annual Return FY 2024‑25: Key Checklist to Avoid Scrutiny

A clear, practical checklist for filing GSTR‑9 for FY 2024‑25. Covers revenue matching, ITC accuracy, RCM compliance, import alignment, reconciliation, and common filing pitfalls to help avoid scrutiny and penalties.

From FY 2024‑25, GSTR‑9 is no longer just a summary form. It’s now a data‑analytics tool used by the GST department to cross‑check your filings. Even small mismatches across GSTR‑1, GSTR‑3B, GSTR‑2B, ICEGATE, and your books can trigger notices, penalties, or blocked ITC.

Why it matters

- Department scrutiny and demand notices

- Blocked input tax credit (ITC)

- Interest and penalty charges

- Alerts for voluntary payments (DRC‑03)

Key areas to double‑check

1. Turnover & sales

- Match revenue across GSTR‑1, GSTR‑3B, and books

- Ensure export/SEZ supplies tally with ICEGATE

- Correctly classify B2B vs B2C sales

- Report e‑commerce supplies properly

2. Input tax credit (ITC)

- ITC in GSTR‑9 must match your books

- Prior year ITC claimed this year should be shown separately

- Blocked ITC (like personal expenses) must be reversed

- Capital goods ITC should not be mixed with regular purchases

3. Reverse charge (RCM)

- Report RCM in the year it’s paid

- Issue self‑invoices for unregistered supplier purchases

- Don’t claim ITC without paying RCM

4. ITC controls (Table 8)

- ITC claimed should not exceed GSTR‑2B limits

- Import IGST must match ICEGATE records

- Apply Rule 42/43 reversals correctly

5. Tax liability & payments

- Extra tax reported in GSTR‑9 must be paid via DRC‑03 (cash only)

- Interest and penalties should match your books

- Supplies of this year but reported next year must be shown in Tables 10–14

6. Exempt & non‑GST supplies

- Report exempt and nil supplies correctly

- Don’t include non‑GST purchases

7. GSTR‑9C reconciliation

- Ensure turnover matches books

- Explain ITC differences clearly

- Disclose stock write‑offs or shortages

8. General compliance

- File GSTR‑9 within 3 years

- NIL return required if turnover > ₹2 Cr but no activity

- Taxpayers ≤ ₹2 Cr are exempt, but filing when exempt may raise questions

Final tip

Think of GSTR‑9 as a cross‑verification tool. Accuracy and proper reconciliation are the only way to avoid scrutiny, audits, and penalties.

FILING YOUR INCOME TAX RETURN F.Y 2024-25 (A.Y. 2025-2026) WITH MYITRONLINE

The income tax filing deadline is right around the corner. If you haven’t filed yet, do it today with Myitronline! Avoid last minute rush and file your tax return today on MYITRONLINE in Just 5 mins.(www.myitronline.com)

If you are looking for eCA assistance to file your income tax return/ GST, you can opt for MYITRONLINE eCA assisted plan starting

Upload Salary Individual Form-16

If you have any questions with filing your tax return, please reply to this mail. info@myitronline.com OR call 9971055886,8130309886.

Note-All the aforementioned information in the article is taken from authentic resources and has been published after moderation. Any change in the information other than fact must be believed as a human error. For queries mail us at marketing@myitronline.com

Krishna Gopal Varshney

An editor at apnokacaKrishna Gopal Varshney, Founder & CEO of Myitronline Global Services Private Limited at Delhi. A dedicated and tireless Expert Service Provider for the clients seeking tax filing assistance and all other essential requirements associated with Business/Professional establishment. Connect to us and let us give the Best Support to make you a Success. Visit our website for latest Business News and IT Updates.

Leave a reply

Your email address will not be published. Required fields are marked *Share this article

Krishna Gopal Varshney

An editor at Myitronline

Krishna Gopal Varshney, Founder & CEO of Myitronline Global Services Private Limited at Delhi. A dedicated and tireless Expert Service Provider for the clients seeking tax filing assistance and all other essential requirements associated with Business/Professional establishment. Connect to us and let us give the Best Support to make you a Success. Visit our website for latest Business News and IT Updates.

View articles

News Offers