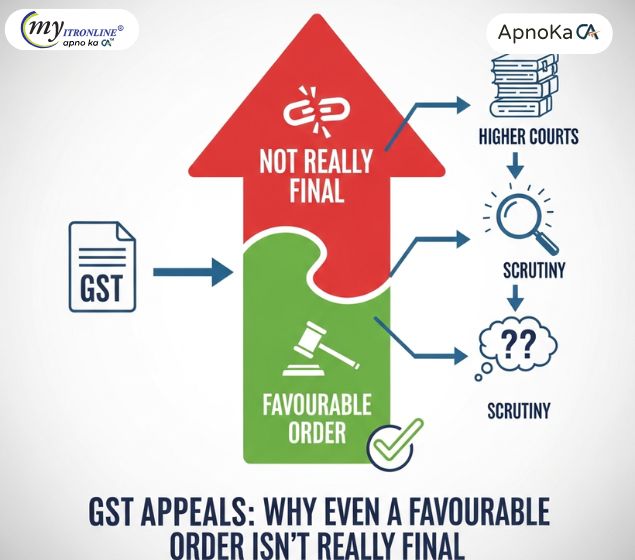

Understanding the GST Exemption for Leasehold Rights Assignment

The recent court ruling on the GST taxation of leasehold rights has given taxpayers much-needed clarification and respite. This important decision exempts leasehold rights from GST as it acknowledges them as immovable property transactions. It gives the potential for reimbursements for previous transactions, lessens the tax burden, and lowers compliance challenges. Examine how this choice promotes ease of doing business while affecting taxpayers and enterprises.

.jpg )

In July 2017, India implemented the Goods and Services Tax (GST) regime with the goal of streamlining the tax code and doing away with cascading levies. Like any thorough reform, it did introduce some uncertainties, especially with relation to the taxation of leasehold rights. Taxpayers now have clarity and relief on this matter, especially in relation to the assignment of leasehold rights, according to a recent court ruling.

Recognizing the Applicability of GST and Leasehold Rights

The conveyance of an interest in real estate through a lease for a predetermined period of time is known as leasehold rights. An upfront payment, sometimes known as a lease premium, paid for the duration of the lease is frequently included in this transfer.

Implications of GST Prior to the Judgment

The categorization and taxation of the assignment of leasehold rights under GST were hotly debated before to the ruling. The main question was whether the leasehold rights assignment amounted to:

- Supply of Goods: Considered a transfer of ownership, this transaction is liable to GST.

- Supply of Services: A transfer of property rights that is considered a taxable service.

- Exempt Transaction: Since transactions involving real estate typically fall outside of GST's purview, this type of transaction is exempt.

Tax authorities have considered these assignments as taxable supplies under GST in a number of situations, which has resulted in substantial tax obligations for both lessors and assignees.

Important Aspects of the Judicial Pronouncement

The Honorable [Name of Court/Authority] defined how leasehold rights assignment is treated under GST in a landmark ruling. The judgment's main points are listed below:

- No "Supply of Goods" Classification: The court decided that the transfer of title to goods is not a part of the leasehold rights assignment. Therefore, under GST, it cannot be categorized as a supply of commodities.

- Immovable Property and Leasehold Rights: The court acknowledged leasehold rights as an immovable property interest. The assignment of such rights was declared exempt from GST as the statute expressly excludes immovable property from its purview.

- Refunds for Past Transactions: The ruling is applicable retroactively, potentially providing taxpayers with a reimbursement for GST paid on previous transactions, subject to the statute of limitations.

- Implications for Compensation Payments: The ruling also made it clear that any payment made in connection with the assignment is not subject to GST as a taxable supply.

Taxpayers' Relief

Taxpayers, particularly those with long-term land and immovable property leases, will greatly benefit from the ruling. Here's how:

- Avoidance of Double Taxation: Since stamp duty and registration fees are already applied to these transactions, taxpayers can now avoid paying GST on top of these fees.

- Clarity for Future Transactions: By helping firms arrange transactions in accordance with GST legislation, the court's clarification will help them avoid litigation and conflicts with tax authorities.

- Tax Burden Reduction: Businesses, particularly those in the infrastructure and real estate industries, will pay less in taxes, which will save money and may result in cheaper costs for customers.

- Encouragement for Ease of Doing corporate: By clearing up this uncertainty, the ruling supports the government's goal of facilitating corporate transactions and cutting down on needless litigation.

Possible Difficulties and Important Considerations

Even while the ruling provides clarity, several issues could still exist:

- Variations in Interpretation: The decision may be applied inconsistently across jurisdictions due to differing interpretations by various state agencies.

- Refund Claims: Taxpayers who want reimbursements for GST paid on previous transactions may encounter delays in filing their claims due to procedural obstacles.

- Application Scope: It may be questioned if the ruling covers all leasehold assignments or just a few (such as residential vs commercial leases).

Procedures for Taxpayers Following a Judgment

To comply with the decision, taxpayers should do the following:

- Examine Previous Transactions: To ascertain eligibility for a refund, examine previous leasehold assignments and evaluate the GST paid on them.

- Update Documentation: To prevent future disagreements, make sure lease agreements and transaction documentation accurately reflect the GST treatment.

- Seek Professional Help: To handle the difficulties of requesting refunds and adhering to the ruling, speak with tax consultants or legal experts.

In Conclusion

Long-standing issues in this area have been resolved by the recent landmark ruling on the transfer of leasehold rights under GST. The judiciary has improved tax law clarity and given taxpayers substantial relief by recognizing leasehold rights as immovable property transactions free from GST.

This is a chance for taxpayers to review their compliance plans, fix any discrepancies from the past, and bring their operations into compliance with the law. The ruling is a much-needed respite for both individuals and corporations as it not only lessens the tax burden but also upholds the principles of fairness and equity in taxes.

FILING YOUR INCOME TAX RETURN F.Y 2024-25 (A.Y. 2025-2026) WITH MYITRONLINE

The income tax filing deadline is right around the corner. If you haven’t filed yet, do it today with Myitronline! Avoid last minute rush and file your tax return today on MYITRONLINE in Just 5 mins.(www.myitronline.com)

If you are looking for eCA assistance to file your income tax return/ GST, you can opt for MYITRONLINE eCA assisted plan starting

Upload Salary Individual Form-16

If you have any questions with filing your tax return, please reply to this mail. info@myitronline.com OR call 9971055886,8130309886.

Note-All the aforementioned information in the article is taken from authentic resources and has been published after moderation. Any change in the information other than fact must be believed as a human error. For queries mail us at marketing@myitronline.com

Krishna Gopal Varshney

An editor at apnokacaKrishna Gopal Varshney, Founder & CEO of Myitronline Global Services Private Limited at Delhi. A dedicated and tireless Expert Service Provider for the clients seeking tax filing assistance and all other essential requirements associated with Business/Professional establishment. Connect to us and let us give the Best Support to make you a Success. Visit our website for latest Business News and IT Updates.

Leave a reply

Your email address will not be published. Required fields are marked *Share this article

Krishna Gopal Varshney

An editor at Myitronline

Krishna Gopal Varshney, Founder & CEO of Myitronline Global Services Private Limited at Delhi. A dedicated and tireless Expert Service Provider for the clients seeking tax filing assistance and all other essential requirements associated with Business/Professional establishment. Connect to us and let us give the Best Support to make you a Success. Visit our website for latest Business News and IT Updates.

View articles

News Offers