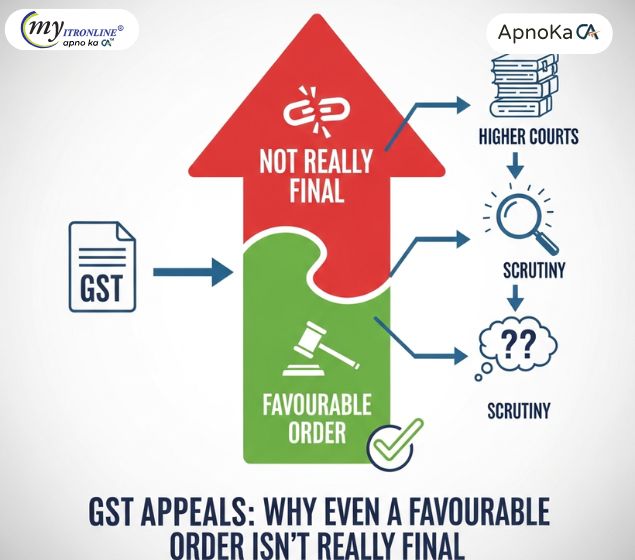

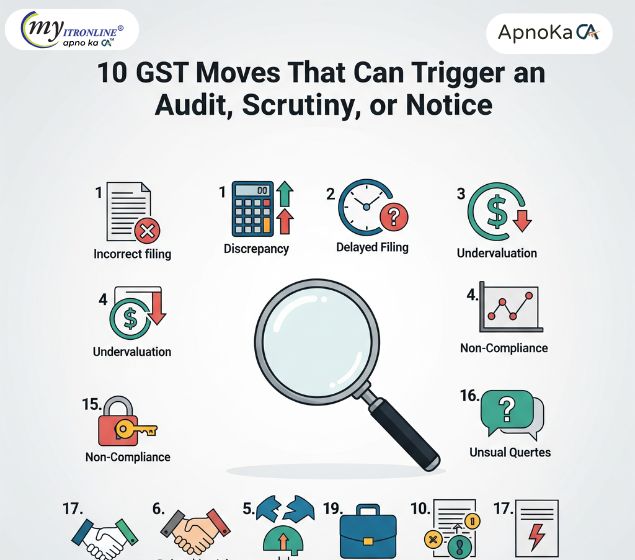

Interest as Exempt Supply: Decoding GST Rules 42-43 for Financial Transactions

This guide outlines how interest income is treated under GST as exempt supply according to Rules 42-43, addressing ITC effects, compliance obligations, and the implications for financial institutions.

.jpg )

Understanding Interest as Exempt Supply: GST Rules 42-43 Explained

In the context of Goods and Services Tax (GST) in India, it's essential for businesses to comprehend what constitutes an exempt supply to ensure adherence and effective tax management. Among various exemptions, interest income is a key subject of conversation. This article explores the clarification surrounding interest as an exempt supply under GST, focusing on Rule 42 and Rule 43.

Defining Exempt Supply

Within the GST structure, "exempt supply" signifies the provision of goods and/or services that are not liable for GST. This category includes supplies that are explicitly exempted, as well as those that fall below the specified turnover threshold. It is important for businesses to determine whether a specific supply falls under this classification in order to accurately compute their tax obligations.

Overview of Rules 42 and 43

The CGST Rules, 2017's Rules 42 and 43 primarily address the apportionment of input tax credit (ITC) among taxable and exempt supplies.

- Rule 42 relates to the distribution of ITC on inputs and input services when a registered individual provides both taxable and exempt goods or services.

- Rule 43 focuses on the apportionment of ITC concerning capital goods utilized for both taxable and exempt supplies.

These rules require that a registered taxpayer adhere to a defined methodology for calculating the ITC that can be claimed, ensuring that businesses do not unduly benefit from ITC linked to exempt supplies.

Clarification on Interest as Exempt Supply

The clarification regarding interest being an exempt supply is crucial for various financial institutions and entities engaged in lending and investment activities. Prior to this clarification, there was uncertainty about whether interest fees on loans, advances, or other financial instruments would qualify as an exempt supply under GST.

Based on the GST Act and subsequent notifications, interest on loans or deposits is generally categorized as part of financial services, which are typically exempt from GST. The following points outline the main aspects:

- Interest's Nature: Interest accrued from loans, advances, or deposits is viewed as income deriving from financial services. Since financial services are classified as exempt supplies under GST, the interest element is also regarded as exempt.

- Consequences for Input Tax Credit (ITC): Given that interest income is classified as an exempt supply, any input tax credit relating to expenses incurred in generating that interest cannot be claimed. Consequently, entities earning substantial interest income should exercise caution when assessing their available ITC, as they must distinctly identify the expenses linked to exempt services.

- Compliance and Documentation: Businesses must keep accurate documentation to validate the exempt status of their interest income. This is crucial during audits and for meeting GST regulations.

- Effects on Financial Institutions: For banks and non-banking financial companies (NBFCs), this classification is important as it influences their overall tax responsibilities and financial strategies.

Conclusion

The clarification that interest income qualifies as an exempt supply under GST, in relation to Rule 42 and Rule 43, carries significant implications for firms engaged in financial services. By grasping the intricacies of these regulations, businesses can ensure proper compliance with GST laws while managing their tax obligations effectively. As the GST landscape continues to evolve, remaining updated about such clarifications will be essential for companies to successfully navigate the regulatory framework.

This article aims to provide a thorough understanding of interest as an exempt supply under GST rules. For businesses impacted by these regulations, seeking professional guidance is crucial to customize the insights to particular operational scenarios and ensure adherence to the most recent laws and amendments.

FILING YOUR INCOME TAX RETURN F.Y 2024-25 (A.Y. 2025-2026) WITH MYITRONLINE

The income tax filing deadline is right around the corner. If you haven’t filed yet, do it today with Myitronline! Avoid last minute rush and file your tax return today on MYITRONLINE in Just 5 mins.(www.myitronline.com)

If you are looking for eCA assistance to file your income tax return/ GST, you can opt for MYITRONLINE eCA assisted plan starting

Upload Salary Individual Form-16

If you have any questions with filing your tax return, please reply to this mail. info@myitronline.com OR call 9971055886,8130309886.

Note-All the aforementioned information in the article is taken from authentic resources and has been published after moderation. Any change in the information other than fact must be believed as a human error. For queries mail us at marketing@myitronline.com

Krishna Gopal Varshney

An editor at apnokacaKrishna Gopal Varshney, Founder & CEO of Myitronline Global Services Private Limited at Delhi. A dedicated and tireless Expert Service Provider for the clients seeking tax filing assistance and all other essential requirements associated with Business/Professional establishment. Connect to us and let us give the Best Support to make you a Success. Visit our website for latest Business News and IT Updates.

Leave a reply

Your email address will not be published. Required fields are marked *Share this article

Krishna Gopal Varshney

An editor at Myitronline

Krishna Gopal Varshney, Founder & CEO of Myitronline Global Services Private Limited at Delhi. A dedicated and tireless Expert Service Provider for the clients seeking tax filing assistance and all other essential requirements associated with Business/Professional establishment. Connect to us and let us give the Best Support to make you a Success. Visit our website for latest Business News and IT Updates.

View articles

News Offers