# gstn

12 posts in `gstn` tag

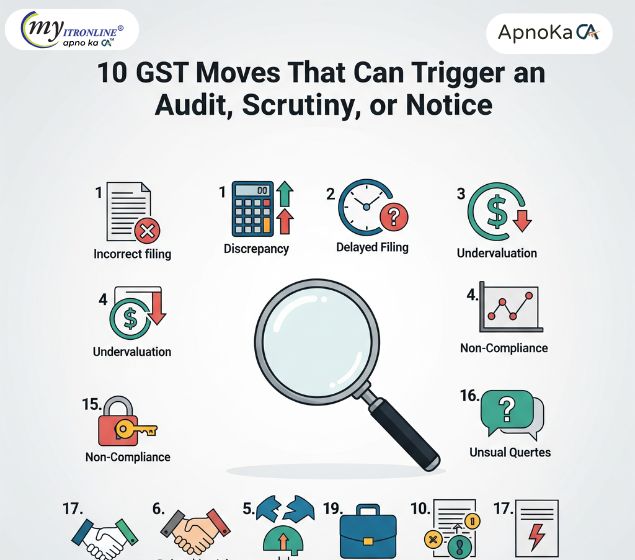

10 GST Moves That Can Trigger an Audit, Scrutiny, or Notice

The GST system uses AI and data analytics to flag discrepancies. This guide details the 10 most common GST mistakes such as excess ITC and GSTR mismatches that instantly catch the department’s eye and lead to notices or audits.

-

By Krishna

Urgent GSTN Alert: Your GST Number Faces Suspension if Bank Details Are Not Submitted

GSTN has issued a strict alert for registered taxpayers: furnish your bank account details on the GST portal within 30 days of registration, or before filing GSTR-1/IFF, whichever is earlier. Non-compliance can lead to suspension via FORM REG-31, blocked GSTR-1 filing, e-way bill generation restrictions, and possible cancellation of registration. To stay compliant, log in to the GST portal, upload your bank details, and ensure verification to keep your GST number active and avoid operational disruptions.

-

By Krishna

Supreme Court’s Big GST Decision Huge Relief for Taxpayers

The Supreme Court of India has ruled that once a taxpayer pays the 10% pre-deposit required to file a GST appeal, the government cannot freeze bank accounts or recover additional funds. This landmark decision protects honest taxpayers and ensures fair enforcement under GST law.

-

By Krishna

GSTN Clarifies: No Change in ITC Auto-Population from GSTR-2B to GSTR-3B

GSTN has issued a clarification confirming that the auto-population of Input Tax Credit (ITC) from GSTR-2B to GSTR-3B remains unchanged, even after the implementation of the Invoice Management System (IMS). GSTR-2B will continue to be generated automatically on the 14th of every month. This update helps clear confusion and reassures taxpayers that their filing process remains stable.

-

By Krishna

Major IMS Enhancements on GST Portal: What Businesses Need to Know

Starting October 2025, the GSTN has rolled out major updates to the Invoice Management System (IMS) that simplify compliance, improve transparency, and give taxpayers more control over invoice handling. This blog breaks down the key changes and what they mean for businesses.

-

By Krishna

Taxpayers Alert: Major Updates in GST Refund Rules

The Goods and Services Tax Network (GSTN) has significantly revamped its refund system, introducing a unified application form (RFD-01), enhanced document uploads, real-time tracking, and integration with PFMS for faster disbursements. This blog details these crucial updates, explaining how they streamline the refund process for taxpayers, promote transparency, and minimize delays, ensuring timely receipt of their legitimate refunds.

-

By Krishna

States Push for Tough Steps to Stop Profiteering from GST Cuts

The GST Council is set to meet on September 3-4 to review GST 2.0 reforms. States want strict rules to prevent profiteering so that GST rate cuts actually benefit consumers. Key proposals include a temporary anti-profiteering law, consumer complaint platforms, and tighter monitoring of sensitive sectors. Businesses, however, warn about compliance costs and pricing disruptions.

-

By Krishna

.jpg)

Important Update for Cancelled Composition Taxpayers Regarding GSTR-3A Notices!

This blog post discusses a common issue for composition taxpayers whose GST registration was canceled before April 1, 2024, or who have already submitted GSTR-4 but received GSTR-3A notices. It explains that these notices result from a system error and can be ignored by the taxpayers affected, meaning no further action is needed. The post also provides guidance on how to raise complaints about other GST-related problems.

-

By Krishna

.jpg)

GSTR-3B Table 3.2: Your Essential Guide to the New Auto-Fill Rules

This blog post breaks down the recent GST Portal advisory about Table 3.2 of GSTR-3B. It explains that starting July 2025, details of inter-state supplies to unregistered persons, composition taxpayers, and UIN holders will be auto-filled and non-editable in GSTR-3B. This information will come directly from GSTR-1 or IFF. The advisory aims to cut down on mistakes and keep data consistent. The post also covers why this change is occurring, how to fix errors by amending GSTR-1/IFF or using GSTR-1A, and offers an action plan for taxpayers to ensure they report accurately and smoothly file their GST.

-

By Krishna

.jpg)

GST Portal Update: Appeal Against Waiver Order (SPL-07) Rejection Now Live!

The GST Portal has introduced a crucial update enabling taxpayers to file appeals (Form APL-01) against rejection orders (SPL-07) issued under the GST Amnesty Scheme. This provides a vital recourse for businesses whose applications for penalty and interest waivers were denied. This detailed guide covers the context of the amnesty scheme, the significance of this new online appeal functionality, critical points to consider before filing (like the 'no withdrawal' policy and pre-deposit requirements), and a comprehensive step-by-step process for filing the appeal on the GST Portal.

-

By Krishna

Easier Reporting: GSTR-7 and GSTR-8 Forms Get Updated!

This blog explains the significant updates to GSTR-7 (TDS) and GSTR-8 (TCS) forms, effective February 11, 2025, aimed at enhancing transaction data detail. It covers the 'why' behind these changes, the expected new reporting requirements (with a crucial note on the GSTR-7 invoice-wise reporting deferment), who is affected, and actionable steps for businesses to prepare for smoother GST compliance and reconciliation.

-

By Krishna

Important GST Update: Act Now! Returns Barred After 3 Years from August 1, 2025

This blog post provides an important update on GST for all registered businesses in India. Starting August 1, 2025, the GSTN will permanently prevent the filing of any GST returns that are more than three years overdue, according to the Finance Act, 2023. The article gives examples, such as GSTR-1 for June 2022 and GSTR-9 for FY 2020-21, to show the impact. It strongly urges taxpayers to reconcile their records right away and file any pending returns. The article discusses the serious consequences of not complying, including losing Input Tax Credit and facing legal troubles. It stresses the need to act now to prevent permanent blocking on the GST portal.

-

By Krishna