# capitalgains

12 posts in `capitalgains` tag

Your Money, Simpler Taxes: Big Changes Coming to the Income Tax Law

The Indian Income Tax Act is evolving rapidly. From the push for the New Tax Regime to AI-driven scrutiny and rationalized capital gains, discover the key trends and anticipated changes that could reshape your financial planning and compliance strategy in the coming years.

-

By Krishna

Capital Gains Accounts Scheme (CGAS) 2025: Major Digital Updates for Taxpayers

The Capital Gains Accounts Scheme (CGAS) has been overhauled for FY 2025-26. Key changes include authorization of 19 private banks (HDFC, ICICI, Axis), acceptance of all major digital payment modes (UPI, NEFT, Cards), online account closure, and the inclusion of Section 54GA (SEZ relocation) exemption.

-

By Krishna

Finally! The 2025 Capital Gains Relief Scheme is Making Life Easier

The 2025 Amendment Scheme has modernised the Capital Gains Account Scheme (CGAS) by making it digital-first and easier to use. Taxpayers can now deposit capital gains online through Net Banking, UPI, RTGS, or NEFT, with the deposit date clearly defined. Electronic statements replace passbooks, more banks are authorised to manage CGAS accounts, and simpler ITR forms are on the way. With broader exemptions like Section 54GA included, the scheme reduces stress and makes compliance smoother for property sellers, NRIs, and businesses.

-

By Krishna

Why Your Tax Refund Is Delayed and What CBDT Wants You to Know

Many taxpayers are waiting for refunds, especially where the refund is large. The Central Board of Direct Taxes (CBDT) is closely checking high-value and flagged returns to stop fake claims and tax cheating. This guide explains the main reasons for delays, which cases get compulsory scrutiny, and simple steps you can take now to clear your refund faster.

-

By Krishna

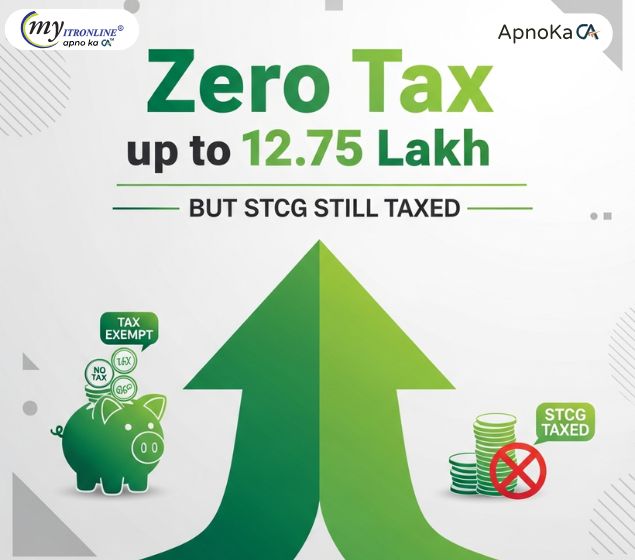

Zero Tax up to 12.75 Lakh But STCG Still Taxed

The Union Budget 2025 has raised the Section 87A rebate, exempting income up to ₹12.75 lakh from tax. However, Short-Term Capital Gains (STCG) on equity shares and mutual funds remain taxable at a flat 15%. While salaried taxpayers enjoy zero tax relief, investors and traders must pay STCG separately without rebate benefits.

-

By Krishna

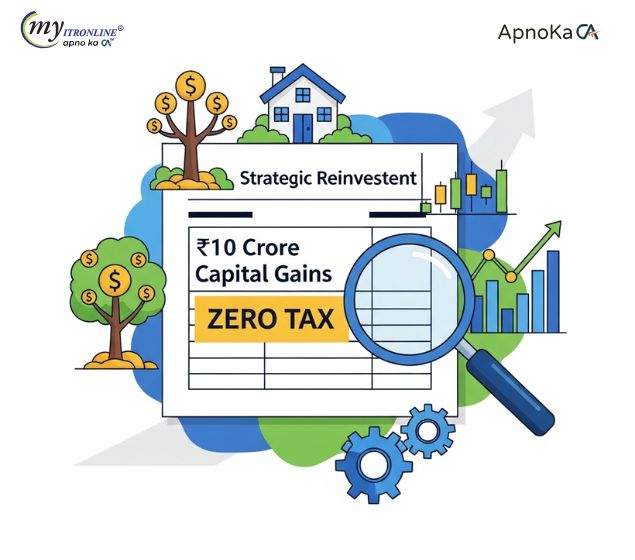

Pay Zero Tax on 10 Crore Capital Gains: Your Guide to Strategic Reinvestment

Selling a big asset like property, stocks, or gold can lead to huge capital gains and a big tax bill. But if you reinvest smartly, you can claim full exemption under Section 54 or 54F, up to ₹10 Crore. This blog explains how to do it, the deadlines, and the rules to follow.

-

By Krishna

Income Tax Benefits for Individuals and HUFs A.Y. 2026–27

A simplified guide to income tax benefits available to Individuals and Hindu Undivided Families (HUFs) for A.Y. 2026–27. Covers exemption limits, rebates, popular deductions, and simplified tax schemes to help taxpayers plan better and save legally.

-

By Krishna

Smart Property Moves: How Sections 54 and 54F Can Slash Your Tax Bill on Residential Property Sales (Latest Rules 2025)

Discover how Sections 54 and 54F of the Indian Income Tax Act provide crucial tax exemptions on Long-Term Capital Gains from property sales. This comprehensive guide covers the latest rules for 2025, including the new ₹10 Crore cap and the two-house option under Section 54, offering practical examples and a step-by-step plan for effective tax planning.

-

By Krishna

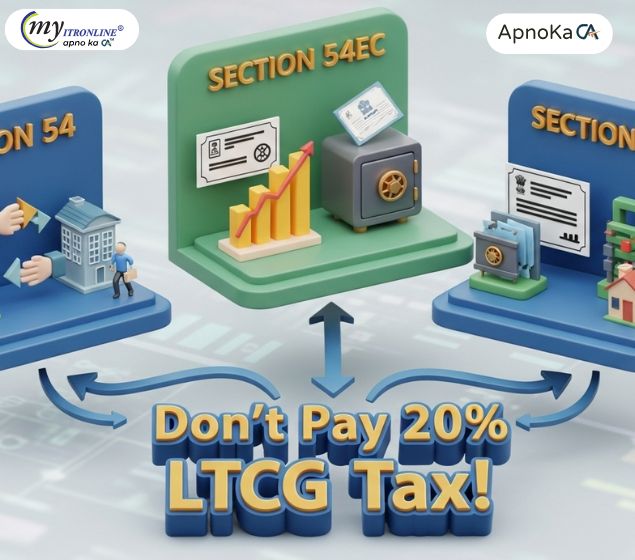

Don't Pay 20% LTCG Tax! How to Use Sections 54, 54EC, 54F

This blog post provides a comprehensive yet easy-to-understand guide to saving Long-Term Capital Gains (LTCG) tax arising from property sales in India. It delves into three crucial sections of the Income Tax Act – Section 54, Section 54EC, and Section 54F – detailing their eligibility criteria, investment options, time limits for reinvestment, and lock-in periods. The post also includes a comparative table and a practical example to illustrate how these exemptions work, empowering taxpayers to make informed decisions and potentially reduce their tax liabilities.

-

By Krishna

New Income Tax Act 2025: Key Updates from the CBDT

The Central Board of Direct Taxes (CBDT) has announced a significant overhaul of the Income Tax Act, effective from assessment year 2025-26. This blog details the crucial changes, including simplified individual tax slabs, revised capital gains taxation, a stronger focus on digital transactions, corporate tax reforms, revamped deductions and exemptions, enhanced anti-evasion measures, and the introduction of a Taxpayer Charter. Understanding these updates is vital for both individuals and corporations to ensure compliance and optimize financial planning under the new regime.

-

By Krishna

.jpg)

A Gift That Keeps on Taxing? ITAT Delivers Key Ruling on Capital Gains Between Spouses

The Income Tax Appellate Tribunal (ITAT) has clarified that when an asset gifted to a spouse is sold, the resulting capital gains must be taxed in the hands of the gifting spouse, not the recipient. This blog breaks down the mandatory "clubbing of income" provision under Section 64(1)(iv) of the Income Tax Act, explaining its implications for taxpayers, the calculation of gains, and the importance of proper documentation.

-

By Krishna

.jpg)

Sold Property in FY 2024–25: Know Tax Rates & Exemptions under Sections 54, 54EC, 54F

A simplified guide for individuals who sold property in FY 2024-25, explaining the tax rates on short-term and long-term capital gains and detailing how to save tax by reinvesting under Sections 54, 54EC, and 54F of the Income Tax Act.

-

By Krishna