# apnokaca

12 posts in `apnokaca` tag

GST Demand Alert: Delhi HC Cancels Duplicate Notices

The Delhi High Court has cancelled duplicate GST demand notices (DRC-07) raised for the same transaction across different financial years, confirming that tax can only be demanded for the year in which the transaction occurred.

-

By Krishna

Understanding Section 112A: Tax Rules for Equity Investors

Section 112A of the Income Tax Act governs taxation of long-term capital gains on listed equity shares, equity-oriented mutual funds, and business trust units. It provides exemption up to 1,00,000 and levies 10% tax beyond that, without indexation benefit.

-

By Krishna

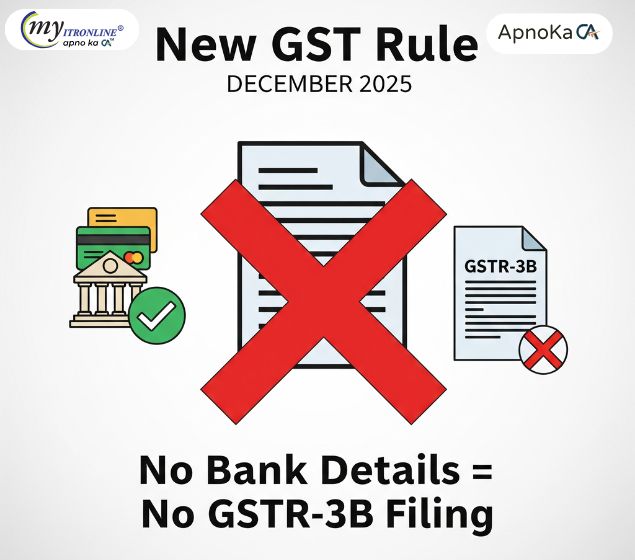

New GST Rule December 2025: No Bank Details = No GSTR-3B Filing

Starting December 2025, GST registrations will face automatic suspension if bank account details are not updated within 30 days or before filing GSTR-1/IFF. This new compliance rule directly impacts filing, billing, and business continuity, making timely updates essential for businesses.

-

By Krishna

GSTR-9 Annual Return FY 2024-25: Avoid Scrutiny with This Checklist

A clear, practical checklist for filing GSTR‑9 for FY 2024‑25. Covers revenue matching, ITC accuracy, RCM compliance, import alignment, reconciliation, and common filing pitfalls to help avoid scrutiny and penalties.

-

By Krishna

GSTR-9 Exemption for Small Businesses: Latest Update Explained

The government has permanently exempted businesses with turnover up to 2 Crores from filing GSTR-9. The move aims to reduce compliance burden while ensuring monthly and quarterly GST filings continue.

-

By Krishna

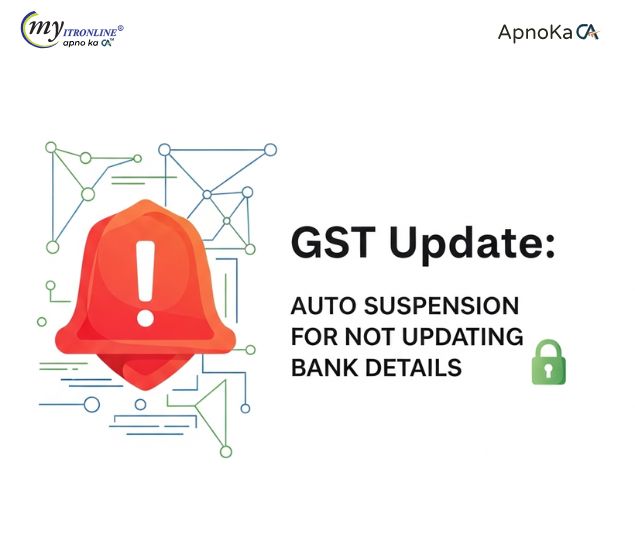

GST Update: Auto Suspension for Not Updating Bank Details

Starting 5th December 2025, businesses registered under GST must update their bank account details within 30 days of registration or before filing GSTR-1/IFF, whichever is earlier. As per Rule 10A, failure to comply will result in automatic suspension of GST registration. The update process requires furnishing bank account number, IFSC code, and a cancelled cheque or bank statement via the GST portal. While OIDAR and NRTP taxpayers are exempt, OIDAR taxpayers with a representative in India must provide bank details. Timely compliance ensures uninterrupted GST registration and avoids cancellation proceedings.

-

By Krishna

Drive Electric, Save on Tax: A Simple Guide to Section 80EEB

A simple guide to Section 80EEB, explaining how individuals can save up to ₹1,50,000 annually on EV loan interest, eligibility rules, and how to claim the deduction under the old tax regime.

-

By Krishna

Why Your Tax Refund Reduced: The Interest You Didn’t Notice

This blog explains in simple language why taxpayers may have to pay extra interest if they delay filing their return, pay less tax during the year, or miss advance tax installments. It breaks down Sections 234A, 234B and 234C in an easy format and shares how timely payments can help avoid extra charges. If your final tax payable is less than ₹10,000, these rules normally do not apply.

-

By Krishna

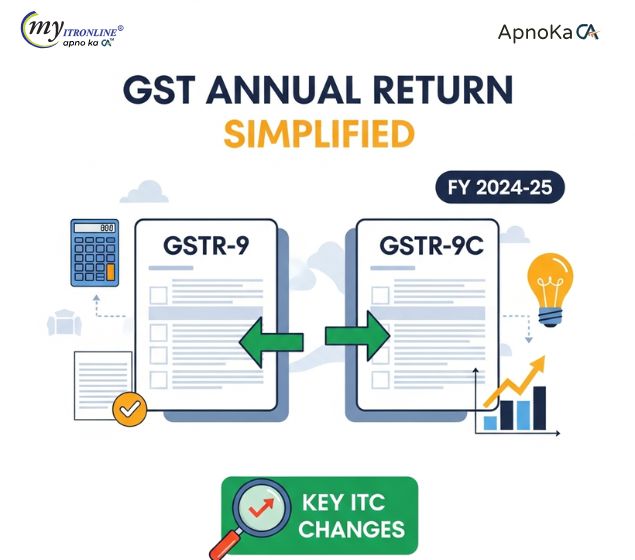

GST Annual Return Simplified: Key ITC Changes in GSTR-9 & GSTR-9C for FY 2024-25

A simplified guide to ITC changes in GSTR-9 and GSTR-9C for FY 2024-25, covering late claims, reversals, reclaims, and reconciliation requirements.

-

By Krishna

CBDT Refund Delay: What Taxpayers Should Know

There is no halt on refund processing by CBDT. Only high-risk refund claims are being held for verification, while smaller refunds are being processed normally. Most legitimate refunds are expected to be released by December.

-

By Krishna

Late Filing of Form 10IC Will Not Deny Lower Tax Rate: ITAT Ruling

Mumbai ITAT has ruled that late filing of Form 10IC should not prevent eligible taxpayers from availing the concessional corporate tax rate under Section 115BAA. The order states that filing Form 10IC is a procedural requirement and the intent to opt for the new tax regime is more important.

-

By Krishna

Advance Tax Alert: December 15th Deadline for AY 2026-27

The next Advance Tax installment for Assessment Year (AY) 2026-27, related to Financial Year 2025-26, is due by December 15, 2025. Taxpayers with total estimated tax liability of ₹10,000 or more after TDS/TCS should pay Advance Tax on time to avoid interest under sections 234B and 234C.

-

By Krishna