Krishna Gopal Varshney

- An editor at apnokaca

Krishna Gopal Varshney Krishna Gopal Varshney, Founder & CEO of Myitronline Global Services Private Limited at Delhi. A dedicated and tireless Expert Service Provider for the clients seeking tax filing assistance and all other essential requirements associated with Business/Professional establishment. Connect to us and let us give the Best Support to make you a Success. Visit our website for latest Business News and IT Updates.

The Latest from Krishna Gopal Varshney

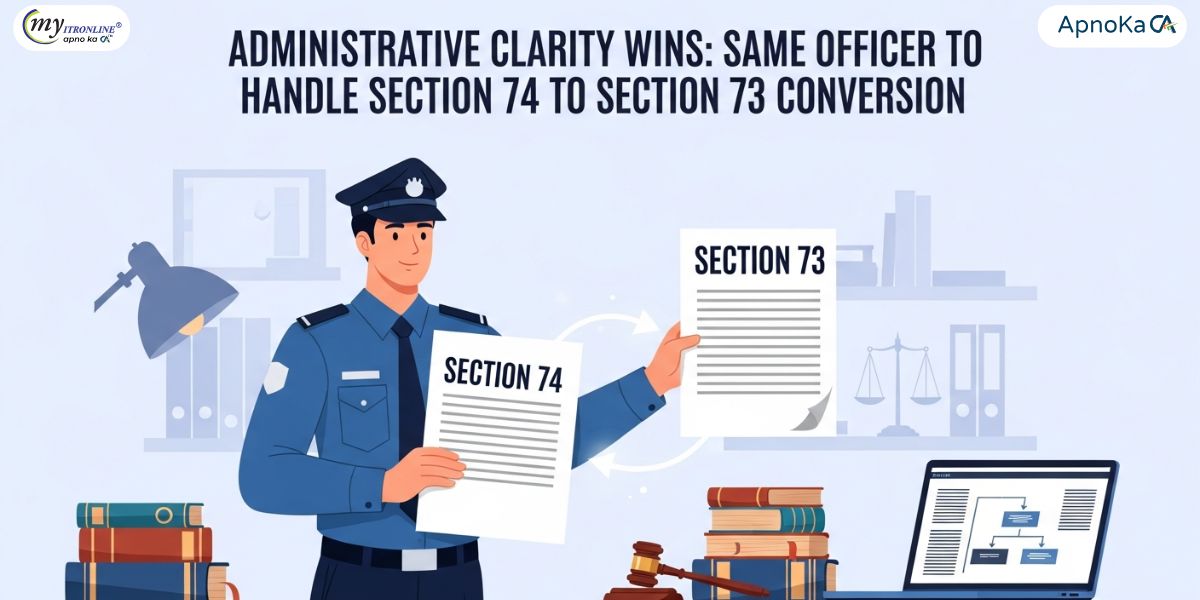

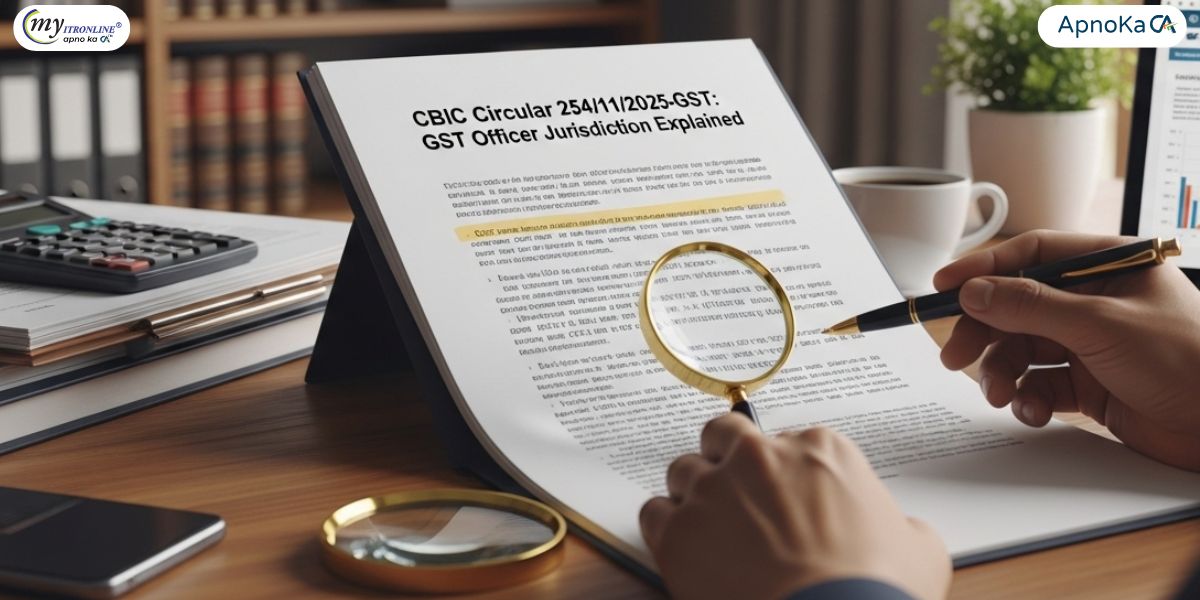

CBIC Circular 254/11/2025-GST: GST Officer Jurisdiction Explained

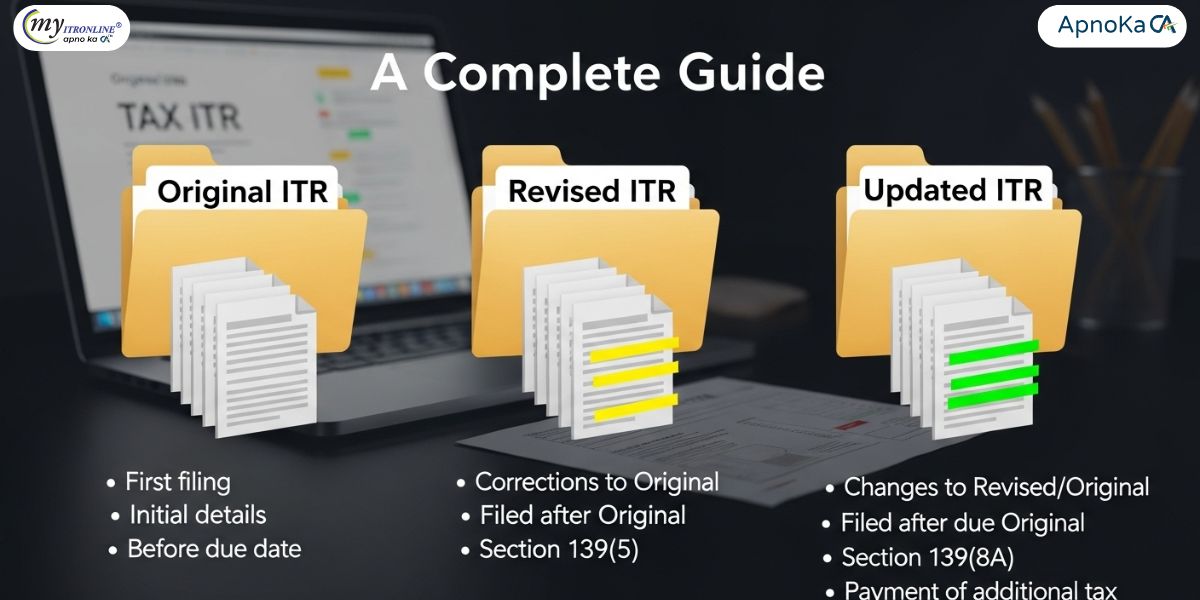

Difference Between Original, Revised, and Updated ITR A Complete Guide

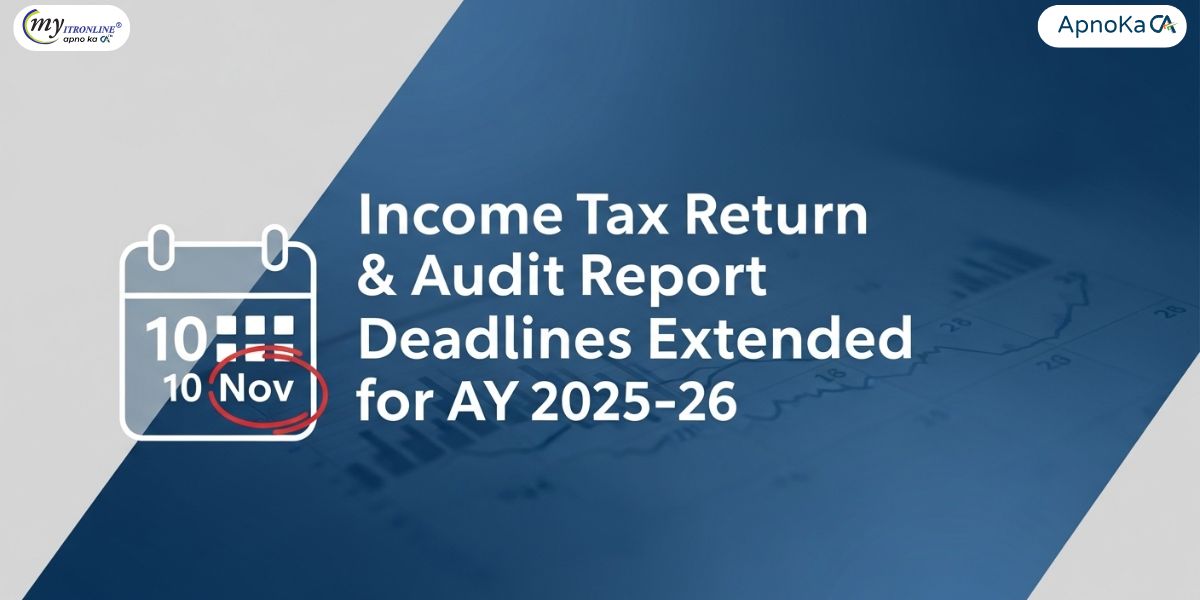

Income Tax Return & Audit Report Deadlines Extended for AY 2025–26

ITR E-Verification Made Easy: Your 2025 Guide Using Demat or Bank Account

Refund Adjusted Against Outstanding Demand: What You Need to Know

Big relief for taxpayers: Supreme Court protects buyers from seller’s default